Part Three: To start your retirement journey

Thinking about stepping into your second innings and making the most of life after 50? If you’re considering retirement, you’re probably wondering where to even begin. Many of you in your fifties are ready to enjoy a more active and rewarding lifestyle, but the first steps can feel a bit overwhelming. While most people focus on finding a steady income right away, there’s a smarter place to start—one that lays the foundation for true peace of mind.

I’ve touched on these steps in my previous article, “Are You Retirement Ready?”, but now let’s take a closer look at step one and explore it in detail. This way, you can move forward with confidence as you plan for a fulfilling new chapter.

Generally, investors tend to think only about one thing: where will their regular income come from during retirement? Is this really the right place to start, though? Personally, I don’t think so. In my view, the starting point is to allocate your current investments such that they meet your pending obligations. These obligations could be unpaid loans or the big expenses that most Indian families have, such as their children’s pending education and wedding expenses.

Why is this even necessary? What happens when people forget to account for these pending expenses?

If you skip this step, you are more likely to overestimate the money you may have for your retirement. Most people tend to believe that they are aware of the amount that they can set aside for retirement. This, however, is generally not the case. Investors tend to only keep in mind the value of their assets and underestimate their liabilities.

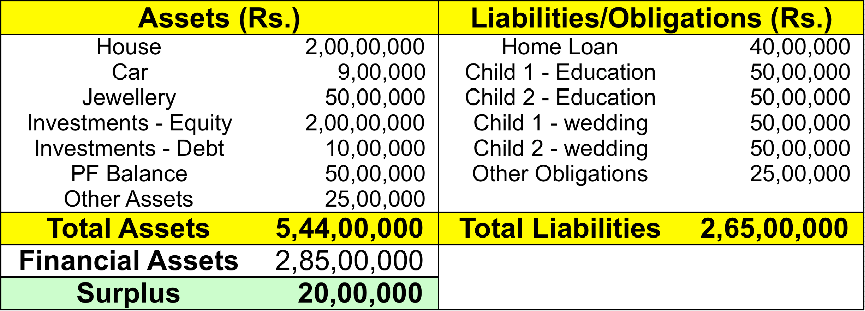

To illustrate my point, let’s take a look at this hypothetical example. In this example, I have put together the assets and liabilities for a typical household. The assets would be property, jewellery, investments, etc. The liabilities and obligations could be outstanding loans and other major obligations.

Household – Assets & Liabilities

Now, as you can see, while the investor might initially believe that they have assets of almost 5.5 crore, they forget that they can only use their financial assets for retirement. After factoring in the pending obligations and debt repayments, one realizes that what is left for retirement may be inadequate or nothing at all! Thus, it is necessary to be clear about which assets are fungible, and having this clarity is what will help you plan well for retirement.

So what are the key takeaways from this?

Step 1: Be Zero Debt

If you are serious about retirement planning, you must first set aside the investments that will be utilized to meet your obligations. Go ahead and prepay your mortgage and any other loans that you have. Ideally, at this stage of your life, your goal should be to simplify life and not have too much complexity around managing loans.

Step 2: Estimate your big obligations as accurately as possible

This is not an easy step. You may not be fully aware of your likely expenses, especially in terms of funding the education of your children or their wedding expenses. So you planned for Rs 50 lacs for your child’s education, and you think it is adequate. What if your child wants to do a 4-year undergraduate in the USA, and if this happens, you would need Rs 50 lacs per year – yes, Rs 2 Cr!

Step 3: Budget for Market Volatility

Even if you have planned for Rs 2 Cr., you do not know what the value of INR: USD will be in the future. What if the Rupee were to depreciate sharply, and you now need an additional Rs 50 lacs?

Let us look at another market scenario. You have the money, but it is not lying idle in the bank; but is invested in an equity mutual fund. The biggest fall in the stock markets was in 2008-09, where the BSE Sensex dropped 60%. What if you were to get caught out in something like this? All your plans would have gone for a toss!

I do not want to scare you or be preachy! I have realised that the biggest problem in Retirement Planning is our inability to estimate the amount required to meet our biggest obligations.

As you gear up for this vibrant new stage, remember: the real key to a smooth transition isn’t just about generating income, but first making sure your major financial obligations are covered. People beyond 50 in their second innings know that a clear picture of assets and liabilities is essential for enjoying the freedom that comes with this age group. By setting aside funds for debts and big-ticket commitments now, you’ll avoid surprises down the road and set yourself up for a more relaxed, rewarding lifestyle. So before you dive into the details of your retirement income, take a moment to get your financial house in order. With a solid foundation, you’ll be ready to embrace all the adventures ahead, on your terms.